"Bikinis, Garbage Loans, And Fishy Finance"

by John Wilder

"The Big Solution to the Great Recession was printing lots of money. I would have (back then) thought that it would have hit the economy all at once. In reality, what the Federal Reserve® and the Treasury did was send all that money they printed off to the banks. The banks didn’t lend it. They kept it on the books, and in fact many of them redeposited their free money with the Fed™. In reality, the Fed© was scared about was the entire system locking up. It was pretty bad in 2009 – basic chemicals that were necessary (say, sulfuric acid) for a basic, functioning economy just stopped production.

No one knew who had money, or who would have money. As one friend of mine noted at the time, “When the tide goes out, you finally see who isn’t wearing swimming trunks.”

The inflation stayed “within target” for the Fed™, flipping up and down around 2% during the decade following. Again, with all of the money printed, I expected it to be more, and I still don’t trust the official government figures on inflation since that would be like trusting a used-car salesman on that gently used 1995 Ford Taurus© with only 350,000 miles on it.

COVID was the final straw, though. People produced less stuff, so there was a lower supply. The government printed a lot more money and then gave it to everyone, who most definitely didn’t save it, and in fact bid prices up on everything. Making nothing and buying everything? Inflation. Or my ex-wife.

Inflation finally triggered interest rates to go up. That posed a problem for the banks. Let’s take me: I have a small mortgage left on Stately Wilder Manor. I’m in no hurry to pay it off because I can get a CD for 5.5%, but my mortgage is only 4%. My mortgage is worth less to the banks now than I owe on it – if I were another bank, they’d sell it to me for less than I owe. That’s a problem for banks that have exposure to mortgages and didn’t sell them off or hedge them.

It’s not just mortgages – Silicon Valley Bank® decided to invest in lots of long-term bonds and such because inflation had been so low. Buy a corporate bond yielding 4%, pay depositors 1%, and profit! But when interest rates started heading upward, the same sort of math as with the bank that owns my mortgage applies – what used to be worth $100 is now only worth, say, $80. Oops. When the people who put hundreds of millions of dollars into the bank, money that wasn’t insured, find out. Bank funs. Er, bank runs.

How bad was it? Of the $172 billion deposited at the bank, only 11% was covered by deposit insurance. I imagine that there were quite a few tense billionaires like Oprah worried that she’d have to get a job at the McDonald’s® drive through, and how could she resist those perfectly salty fries? Since billionaires were in danger, the FDIC immediately said, “Rules? Who needs those. All money is safe in Bartertown!”

My initial expectation is that we’d see more bank failures right around now as interest rates increased and the piles of garbage on the balance sheets of the banks started to rot. Instead? Banks are still (I believe) happily lending money borrowed by the Fed™.

How do they do it? They manage to do it by having the Fed© allow them to mark their assets to what they paid for them, not what they’re worth. So, they’re lying. I’m fairly certain the Fed™ is buying this stuff to get it off the balance sheets of the banks and lending them more money whenever they don’t have enough caviar.

The rot, though, is still there – it’s only a matter of who pays for the rot. Debt always gets paid, the old saying goes, either by the borrower or by the lender. I do know of two local businesses that are going bankrupt. Their debt is what drove the bankruptcy. My guess is that, combined, they have a debt of a million and a half dollars (or so). Who will pay it? In the end, the lender will.

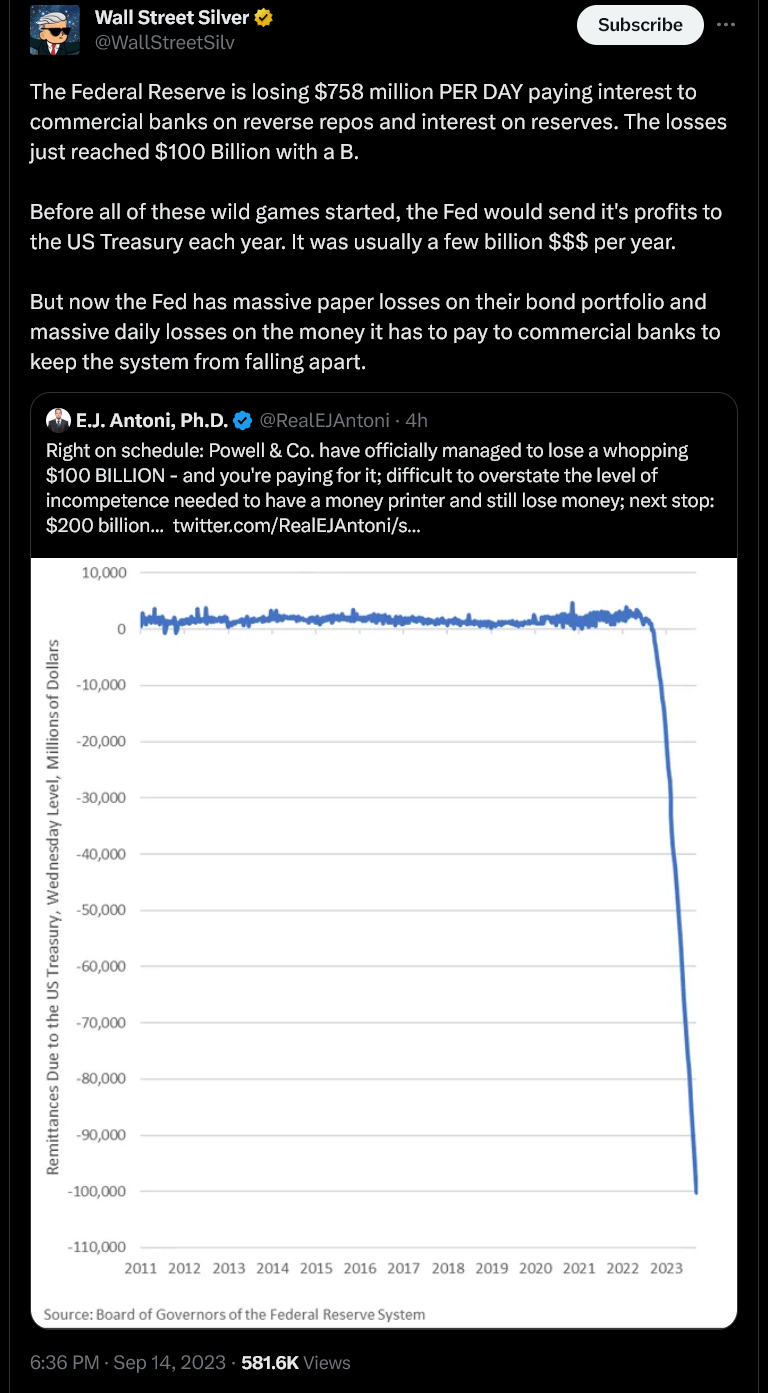

I think that might be at least part of the big jump in debt that the United States owes. As interest rates go up, Uncle Sam is acting like a raccoon and jumping straight into the trash can to eat the garbage loans and bonds that the banks had to throw out because they were stinking up the fridge. Here’s proof:

Eventually, printing lots and lots of money is like a magic trick the magician does one too many times and everyone sees how it works. Will it work this time? Unrelated, frequent commenter Ray notes this Give Send Go. I'll let him explain more. GiveSendGo - "Loco Needs Divorce from Prostate: The Leader in Freedom Fundraising."

No comments:

Post a Comment