"Heaven And Hell"

by Bill Bonner

From banking crises to our chapel on

the ranch, a look at solid foundations

San Martin, Argentina - "As predicted…when the fight gets tough, the Fed takes a dive. That is what we are watching now…in slow motion. After the crisis of ’08, the feds insisted that the banks hold more reserves. They were told to buy safe, government debt – T-bonds. The Treasuries were supposed to be financial ballast, designed to keep them safe in a market squall.

Oh, if only Mother Nature, in all her guises and disguises, would cooperate! A storm blew up last week. Now loaded up with Treasury debt, banks are much more solid – on paper – than they were in 2008. But what happened? The ballast sank. And two banks sank with it.

Foxes in the Henhouse: The California bank, Silicon Valley Bank, has a CEO, Greg Becker, who was also a director of the San Francisco Fed. The New York bank, Signature, has none other than Barney Frank, who, along with Elizabeth Warren, actually wrote key parts of the 2010 bank regulations.

But neither regulators nor regulations saved them. As interest rates rose, fixed-return assets, notably bonds, were not as valuable as they had been before. Two years ago, you could get only a 1.5% yield from your 10-year Treasury. Today, the yield is 3.7%. The income stream from the old bond is now worth only half as much as it was. Which means, the value of the banks’ reserves – their balance sheets – fell. As this continues, more banks can be expected to get into trouble. And the Fed will have to bail them out. Or give up its interest rate hikes altogether.

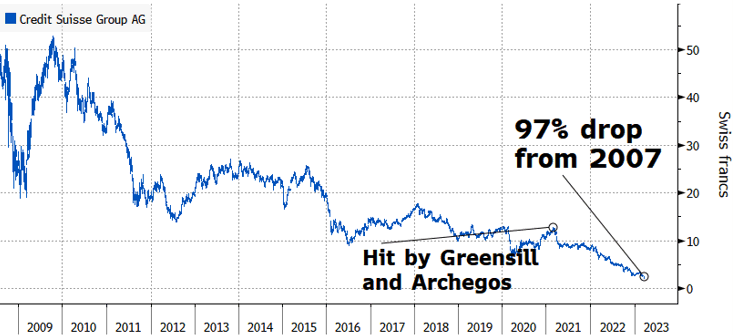

One big bank that people are watching is Credit Suisse. Naked Capitalism: "Silicon Valley Bank Fallout Nudges World’s Most Troubled Systemic Lender, Credit Suisse, Closer to Edge" ...despite losing over 95% of its market value since 2008, it is still too big to fail.

The shares of Credit Suisse Group AG, the world’s most troubled systemic lender, fell by as much as 15% on Monday (March 13) to another fresh record low, before recovering slightly in the latter hours of trading. They are down a further 4% so far today (12pm CET, March 14). This latest crisis of confidence in global banking has also fueled a fresh surge in the cost of insuring CS’s bonds against default. The five-year credit default swaps on CS’ debt surged to a new record of 453 basis points on Monday. It was the widest move of 125 European high-grade companies tracked by Bloomberg.

Will Credit Suisse be next? Will it push investors and the Fed into a panic? Will the Fed publicly reverse course and begin cutting rates? We don’t know…we’ll await events.

An Honest Day’s Work: Meanwhile, our 14-year-old grandson is visiting. The boy lives in the suburbs in the US with little opportunity to get out beyond the reach of Iphones, Ipads, Tik Toks, video games and whatever else it is that occupies the time and attention of American youth. His parents say he is bored by school and developing ‘a teenager attitude.’

We decided the best thing might be just to put him to work. Physical work. As long-time sufferers of our ‘blog’ know, we do not play golf…or hunt…or hang out with friends. We have no TV. And on weekends, we avoid opening our computer, if we can manage it. Instead, we find projects that require physical activity…and give us something to show for our time. Carpentry. Masonry. Painting. We do it all – badly.

(Chapel, rear view. Source: Bill)

A couple of years ago, down here at the farm, we began building a tiny family chapel. It is built of adobe blocks, just as all the churches in the area are, with a cross – illuminated by the sun – made of wine bottles.

(In vino veritas. Source: Bill)

A couple of years ago, down here at the farm, we began building a tiny family chapel. It is built of adobe blocks, just as all the churches in the area are, with a cross – illuminated by the sun – made of wine bottles.

The other odd thing about it is the roof. We began by making four arches of reinforced concrete, to form a square at the base. This is not at all traditional, but it guarantees the solidity of the structure.

Chapel, side view. Source: Bill)

“Good idea,” said a former owner, now neighbor. “The old house was largely destroyed by an earthquake in the 1920s.”

Adobe walls were laid up on all four sides, about a foot outside the concrete arches. Why the gap between the arches and the walls? We don’t remember. The plans were sketched out on a piece of paper…and then lost. Maybe the idea was just to give it, from the inside, a more complex and more interesting form.

A vaulted roof was fashioned out of barrel staves that we took from some long-abandoned oak wine barrels. The barrel wood, set on top of the concrete arches gave us the bones of the roof. The flesh of it was made from small cane, laid down on top of the barrel staves…and covered with mud. It rains very little here, so the same mud was used to make the adobe bricks as well as the roof itself.

A Solid Foundation: All in all, we were pleased with how it turned out. But when we left last year, it was still unfinished…so we returned this time with work still to do – the floor. There were some blocks of very hard wood – quebracho – left over from a floor in the house. The blocks are heavy and almost impossible to cut, but they make a nice surface when they are polished. There aren’t enough of them to do the entire floor, so we will use them to make a border around the edge of the chapel floor…and a cross in the center.

We began on Saturday, using our grandson as a ‘hod carrier’ and ‘mud boy.’ We showed him how to ‘screen’ the sand to remove the pebbles. Then, he learned how to mix it with lime in a wheelbarrow, add water, and end up with a creamy consistency. “Grandad, can I lay down the blocks?” “I don’t know…it takes some real skill. The blocks are not all the same size. You’ve got to make sure they come out flat on top.”

We showed him how to put down a bed of mortar…making ridges in it to give it some squishability. And then we tapped the block down with a hammer until the top of it lined up with the other blocks. “I can do it, Grandad.”

The first row of blocks we laid down weren’t the best. They had to be taken up and re-done. It was a mistake, we discovered, to try to line them up with the wall. The base of the wall was made out of stone, which keeps the mud bricks up off of the ground. But it is irregular. “How did you learn to do this, Grandad?” “Oh…I’m an autodidact.” “A what…?” “It means I learned on my own.”

“You mean by trial and error.” “Mostly error. But that’s the way you learn everything. Either your mistake or someone else’s. But the nice thing about life is that it corrects errors…whether you like it or not. ” “What’s the problem in school,” we asked. “Oh…it’s just boring. I want to drop out.” "What would you do instead?” “I don’t know. Nothing, I guess.” “That doesn’t sound very interesting. But if you want to drop out of school you could help me. We could do this kind of work every day.”

We were working inside, but on our knees. And the day was hot. After a while, the enthusiasm for manual labor began to wane. “How long are we going to do this, Grandad?” “Until they call us for dinner.” “But I’ve got to study my Spanish.” “We’ll, how about finishing this row, then you can go study.” “Okay…” The results were so-so. But they will give the old man cover for his own sloppy work. “Yeah…they’re a little uneven,” we’ll admit. “I let my grandson do it.”

.jpeg)

{kind=link}